Case for Portfolio Exposure to the Middle East – The Last Frontier: As global fund managers allocate assets for 2011, there is a case forMiddle East to be treated as a separate asset class. Asian countries included in the frontier markets like Vietnam and Indonesia have higher correlations to the China and East Asian markets. Gulf Cooperation Council (GCC) / Middle Eastern markets have heavier reliance on crude oil prices, a different place in economic development, cycle-distinct cultures, the distinct nature of retail investors, index investability and float.

This is even more true, due to the fact that GCC Is the world’s largest producer of crude oil. The value of ME crude oil resources is at $18.3 trillion, with a present value of $11.2 trillion, assuming a 3% rate of return (and discount rate) and a price of $50 per barrel; GCC natural gas reserves would be $5.1 trillion, assuming a discount rate of 3% and a price of $5 per million BTU -- which, combined, is higher than U.S. GDP.

The value of oil reserves increases to $37 trillion, assuming a crude oil price at $80 / barrel with a 3% discount rate, and a value of natural gas reserves at $7.8 trillion at a natural gas price of $7 / MMBTU and 3% discount rate -- which is higher than total global private wealth, at $38 trillion. If oil prices were to average $100 per barrel and gas $10, the present value of GCC energy reserves would be $60.7 trillion, equal to the world's total stock market capitalization.

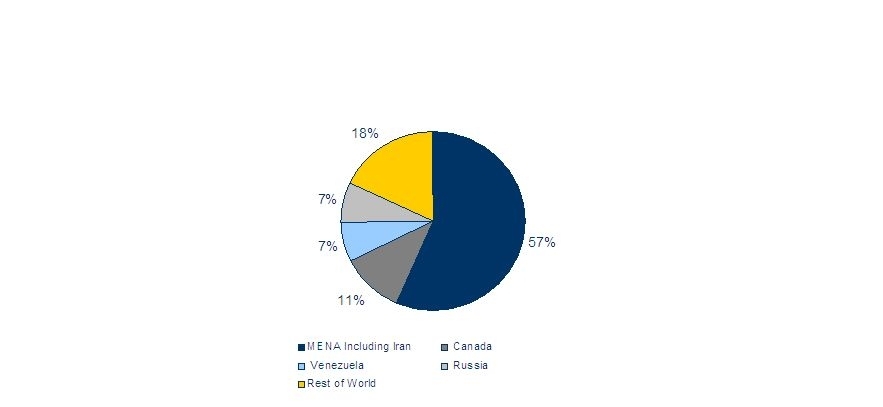

This energy commodity wealth is sufficient to finance the transformation of GCC countries into diversified economies through investments in infrastructure and education. The chart below gives an estimated share of GCC in global oil reserves.

[Click all to enlarge]

No comments:

Post a Comment