By Valentina Romei and Ranjit Lall

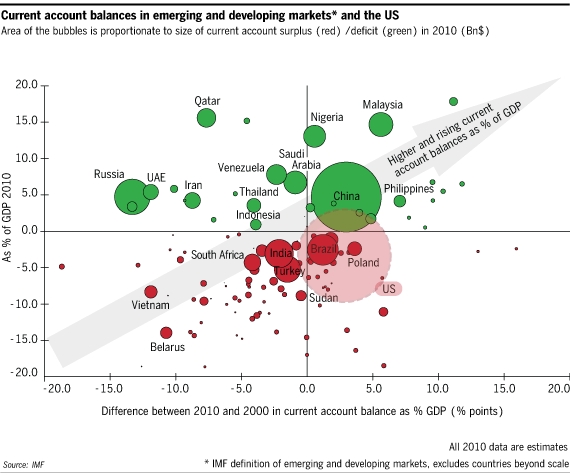

The debate on global imbalances often revolves around China’s gigantic current account surplus. Yet as this week’s beyondbrics chart (after the break) shows, on the most meaningful economic measure of size - the current account balance as a percentage of GDP - China’s surplus is smaller than many of its emerging market peers. Whether that point will be recognised in debates over the global economy atthis week’s G20 meeting in Seoul is another matter.

Countries above the horizontal axis on the chart run surpluses and those below have deficits. The bigger the circle, the larger the balance is in absolute terms. The further the country is from the horizontal axis, the larger the balance as a proportion of GDP. The further it is from the vertical axis, the more its balance has grown or shrunk in the past decade.

To be sure, the absolute size of China’s surplus ($270bn in 2010) is striking. It’s roughly equal to the sum of the next ten largest surpluses combined. Given the enormity of the US’s deficit (the dotted line circle), it is little surprise that the debate on global imbalances has turned into a slanging match between the US and China.

But as a percentage of GDP, the measure most commonly used by economists, China’s surplus is not particularly large. At 4.7 per cent of GDP, it only marginally breaches the 4 per cent cap on current account balances proposed by US Treasury secretary Tim Geithner last month. China curtly dismissed the proposal anyway, saying it harked back “to the days of planned economies”.

A quick glance at the chart corrects another common misperception: that emerging markets mostly run current account surpluses. Two of the Brics - India and Brazil - run deficits, as do a number of second tier emerging markets such as South Africa and Turkey. The countries running current account surpluses, as one would expect, tend to be major commodities exporters.

Nor is it true that these surpluses and deficits have been growing over the last 10 years. Most balances have shrunk. This is most pronounced in Russia, whose surplus has declined by almost 15 percentage points. Even oil exporters such as Qatar and Saudi Arabia have seen their surpluses fall, largely due to the oil price collapse in 2008. China is a big exception - even though its surplus is lower than its pre-crisis high of 10 per cent of GDP - which partly explains why it has come under so much pressure.

All of this calls for a nuanced view of emerging market current accounts. Despite its prominence in the debate on global imbalances, China is not representative of most emerging markets. Both investors and policymakers would do well to remember this.

This feature appears every Monday on beyondbrics, presenting a chart that tells the story of a current economic or financial issue from emerging markets

No comments:

Post a Comment