"Under Shariah, or traditional Islamic law, charging interest on a loan is taboo, but Muslim businessmen have created sukuk, which are financial instruments that can enable a return on principal. Less than a year ago, during the worst days of Dubai's financial crisis, it seemed likely that lawyers would turn Dubai into a laboratory for thrashing out the consequences of defaulting sukuk. Now, though, the worst of the financial crisis in Dubai has passed, with a minimum of such thrashing.

According to Mohammad Saeed Rahman, founder of Portland Oregon's Institute of Halal Investing, Dubai has turned the corner, and government-controlled company Dubai Holdings 'will satisfy its bondholders with hybrid payments, 30% to 40% in cash, and issuing new securities for a longer period of time to restructure the remainder of the debt.'

While the worst of the crisis may be past for the emirate, Dubai has highlighted some issues underlying the Islamic world's integration with worldwide finance. The rejection of riba (translated from the Arabic as 'usury' or 'interest') and the rejection of gharar (translated as 'the sale of uncaught fish,' which indicates risky trading) are among the defining principles of Shariah finance. So the question emerges: how can sukuk avoid riba or gharar?"

Monday, 8 November 2010

Aluminium Bahrain prices IPO at BD0.900 per share - Banking & Finance - ArabianBusiness.com

Aluminium Bahrain (Alba) has priced the institutional tranche of its initial public offering (IPO) at BD0.900 per share, its largest stakeholder Mumtalakat said on Monday.

The final price of the IPO, which saw the fund float 142 million ordinary shares, was determined through a bookbuilding process, Mumtalakat said in a statement.

The state-backed fund, which owns 77 percent of Alba, said in October it planned to raise up to BD204m ($530m) in the IPO as it diversified away from local investments.

The final price of the IPO, which saw the fund float 142 million ordinary shares, was determined through a bookbuilding process, Mumtalakat said in a statement.

The state-backed fund, which owns 77 percent of Alba, said in October it planned to raise up to BD204m ($530m) in the IPO as it diversified away from local investments.

Dubai: more entrepreneurs please | beyondbrics: News and views on emerging markets | FT.com

Martin Lukes, the FT’s fictional business-leader (now sadly deceased), would have loved the Celebration of Entrepreneurship conference being held this week in one of Dubai’s plushest convention centres.

Guests have been discouraged from wearing suits and ties to reflect the “unconventional and energy generating” atmosphere, and invited to attend “passion corners”. Speakers will share inspiring stories in an “informal, highly interactive and unencumbered” setting. But the conference’s faddish presentation belies its serious subject: how can the Arab Gulf help aspiring entrepreneurs?

Currently, the environment for start-ups is tough. Governments are all-powerful, long-established merchant families dominate the private sector, and - paradoxically for such a wealthy region - financing is almost impossible to drum up.

Guests have been discouraged from wearing suits and ties to reflect the “unconventional and energy generating” atmosphere, and invited to attend “passion corners”. Speakers will share inspiring stories in an “informal, highly interactive and unencumbered” setting. But the conference’s faddish presentation belies its serious subject: how can the Arab Gulf help aspiring entrepreneurs?

Currently, the environment for start-ups is tough. Governments are all-powerful, long-established merchant families dominate the private sector, and - paradoxically for such a wealthy region - financing is almost impossible to drum up.

Dubai's Union Properties finalises hotel sale - Maktoob News

Dubai's Union Properties has finalised the sale of its Ritz Carlton hotel in the Gulf emirate for 1.1 billion dirhams ($299.6 million) and use the money to reduce debt and complete remaining projects.

The hotel, located at the Dubai International Financial Centre, will now be owned by a private company based in Abu Dhabi, Union Properties said in a statement. The property firm did not reveal the name of the hotel's new owners.

"The proceeds generated from the transaction will be directed toward reducing the company's overall debt position and completing few remaining assets at our flagship development, the MotorCity," said Khalid AlJarwan the general manager for Union Properties.

The hotel, located at the Dubai International Financial Centre, will now be owned by a private company based in Abu Dhabi, Union Properties said in a statement. The property firm did not reveal the name of the hotel's new owners.

"The proceeds generated from the transaction will be directed toward reducing the company's overall debt position and completing few remaining assets at our flagship development, the MotorCity," said Khalid AlJarwan the general manager for Union Properties.

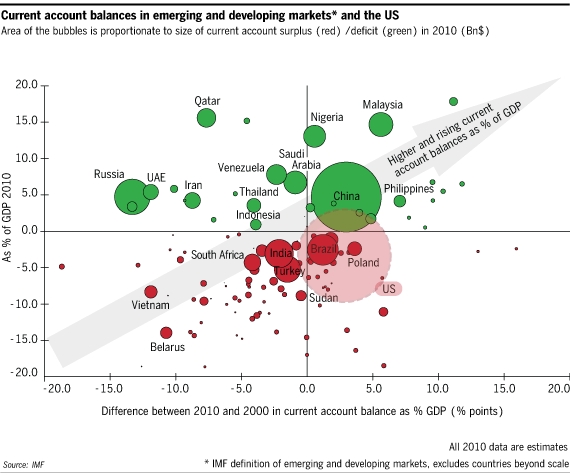

Chart of the week: China’s surplus not as big as it seems | beyondbrics: News and views on emerging markets | FT.com

By Valentina Romei and Ranjit Lall

The debate on global imbalances often revolves around China’s gigantic current account surplus. Yet as this week’s beyondbrics chart (after the break) shows, on the most meaningful economic measure of size - the current account balance as a percentage of GDP - China’s surplus is smaller than many of its emerging market peers. Whether that point will be recognised in debates over the global economy atthis week’s G20 meeting in Seoul is another matter.

Countries above the horizontal axis on the chart run surpluses and those below have deficits. The bigger the circle, the larger the balance is in absolute terms. The further the country is from the horizontal axis, the larger the balance as a proportion of GDP. The further it is from the vertical axis, the more its balance has grown or shrunk in the past decade.

To be sure, the absolute size of China’s surplus ($270bn in 2010) is striking. It’s roughly equal to the sum of the next ten largest surpluses combined. Given the enormity of the US’s deficit (the dotted line circle), it is little surprise that the debate on global imbalances has turned into a slanging match between the US and China.

But as a percentage of GDP, the measure most commonly used by economists, China’s surplus is not particularly large. At 4.7 per cent of GDP, it only marginally breaches the 4 per cent cap on current account balances proposed by US Treasury secretary Tim Geithner last month. China curtly dismissed the proposal anyway, saying it harked back “to the days of planned economies”.

A quick glance at the chart corrects another common misperception: that emerging markets mostly run current account surpluses. Two of the Brics - India and Brazil - run deficits, as do a number of second tier emerging markets such as South Africa and Turkey. The countries running current account surpluses, as one would expect, tend to be major commodities exporters.

Nor is it true that these surpluses and deficits have been growing over the last 10 years. Most balances have shrunk. This is most pronounced in Russia, whose surplus has declined by almost 15 percentage points. Even oil exporters such as Qatar and Saudi Arabia have seen their surpluses fall, largely due to the oil price collapse in 2008. China is a big exception - even though its surplus is lower than its pre-crisis high of 10 per cent of GDP - which partly explains why it has come under so much pressure.

All of this calls for a nuanced view of emerging market current accounts. Despite its prominence in the debate on global imbalances, China is not representative of most emerging markets. Both investors and policymakers would do well to remember this.

This feature appears every Monday on beyondbrics, presenting a chart that tells the story of a current economic or financial issue from emerging markets

Dubai Shares Drop as DFM Posts Loss, Raising Concern October Gain Overdone - Bloomberg

Dubai shares retreated to the lowest level in a month as Dubai Financial Market PJSC reported a third-quarter loss, raising concern that the benchmark’s gain of almost 5 percent in October was overdone.

Dubai Financial Market decreased the most since March as it posted a loss of 2.95 million dirhams ($803,000). Drake & Scull International PJSC, an engineering contractor for the real- estate industry, declined 1.3 percent after profit fell 44 percent amid rising costs. The DFM General Index slipped 1.7 percent to 1,693.3, the lowest since Oct. 5, at the 2 p.m. close in Dubai. The measure gained 4.8 percent in October.

“Markets have been very strong, so this is a bout of profit-taking,” said Sebastien Henin, portfolio manager at The National Investor in Abu Dhabi. “The DFM reported poor results and some investors were disappointed.” Arabtec Holding Plc’s third-quarter earnings also drove the decline, he said.

Dubai Financial Market decreased the most since March as it posted a loss of 2.95 million dirhams ($803,000). Drake & Scull International PJSC, an engineering contractor for the real- estate industry, declined 1.3 percent after profit fell 44 percent amid rising costs. The DFM General Index slipped 1.7 percent to 1,693.3, the lowest since Oct. 5, at the 2 p.m. close in Dubai. The measure gained 4.8 percent in October.

“Markets have been very strong, so this is a bout of profit-taking,” said Sebastien Henin, portfolio manager at The National Investor in Abu Dhabi. “The DFM reported poor results and some investors were disappointed.” Arabtec Holding Plc’s third-quarter earnings also drove the decline, he said.

Gulf Issuers Skip Sukuk to Tap Demand for Emerging Debt: Islamic Finance - Bloomberg

Persian Gulf issuers are choosing to sell non-Islamic bonds instead of sukuk in the borrowing rush that has followed Dubai World’s debt restructuring.

Non-Islamic bond sales from the region may almost double to $15 billion this quarter as companies from Qatar National Bank SAQ, the country’s largest bank, to Oman-based MB Petroleum Services LLC tap the market, investment bank Exotix Ltd. in Dubai estimates. The $1 billion Shariah-compliant bond sale by Saudi Aramco and Total SA is the only announced sukuk sale for the rest of 2010.

The abundance of liquidity in the non-Islamic debt market, the enforceability of investors’ rights in defaults and the extra cost associated with Islamic bond documentation are steering issuers away from sukuk, Unicorn Investment Bank BSC’s senior vice president of capital markets, Nida Raza, said Nov. 2.

Non-Islamic bond sales from the region may almost double to $15 billion this quarter as companies from Qatar National Bank SAQ, the country’s largest bank, to Oman-based MB Petroleum Services LLC tap the market, investment bank Exotix Ltd. in Dubai estimates. The $1 billion Shariah-compliant bond sale by Saudi Aramco and Total SA is the only announced sukuk sale for the rest of 2010.

The abundance of liquidity in the non-Islamic debt market, the enforceability of investors’ rights in defaults and the extra cost associated with Islamic bond documentation are steering issuers away from sukuk, Unicorn Investment Bank BSC’s senior vice president of capital markets, Nida Raza, said Nov. 2.

Debts from the boom still hang over Dubai and Abu Dhabi � ArabianMoney

Speculation by Bank of America Merrill Lynch that Aldar Properties now needs to raise an additional $2.7 billion in debt is a reminder that Dubai was not the only emirate to pile on debt in the boom, albeit the $42.3 billion estimated to be repayable by Dubai over the next two years dwarfs this amount.

Analysts do not expect a repeat of the Dubai debt crisis of almost a year ago when it looked as if there might be a default on Nakheel bonds. Both emirates have learnt from that PR disaster and relations between the two have seldom been on a better footing.

UAE unity rules

Rather than disunite the United Arab Emirates there has been a new awareness of collectice self-interest, or to be more frank a realisation that Dubai and Abu Dhabi sink or swim together.

How difficult then is the task that lies ahead? Dubai raised a $1.25 billion bond on international markets at the end of September, and both Emaar Properties and Dubai Electricity and Water have also raised money in bond markets.

But then let us not forget the financial position of Abu Dhabi, arguably the world’s richest city. There is $450-650 billion in its sovereign wealth funds; $3-4 trillion worth of oil in the ground which makes the average family worth $100 million plus; and the cash flow from the rising oil price.

The anomaly was surely that Dubai and Abu Dhabi used to operate entirely without debt in the past, simply using oil revenues and retained business profits to fund investments in infrastructure. Both cities could have grown even faster by borrowing and took a very conservative approach.

More Abu Dhabi bond issues

To refinance the UAE is surely not really a problem with all that wealth to hand. Abu Dhabi needs to issue bonds to recapitalize the debts. That is what happened in the Dubai debt crisis a year ago.

But as analysts point out there will always be strings attached, and clearly Dubai would like to keep as much as it can. However, there may come a tipping point when it is obvious that the objective of getting the show back on the road quickly supercedes a longer term outlook, or indeed becomes imperative to secure the long-term.

The upcoming $42.3 billion in short-term debt will surely focus attention, as has the alleged $2.7 billion funding gap has at Aldar Properties. For wiping the slate clean after the recent boom would be in the interest of all parties, and it will happen sooner or later.

Ironically while Bank of America Merrill Lynch has highlighted Aldar’s problems, the bank itself is the subject of intense speculation about the viability of its own balance sheet (click here). These are still difficult times for financial markets and only the players with the strongest financial backing will ultimately survive.

Posted on 08 November 2010

Analysts do not expect a repeat of the Dubai debt crisis of almost a year ago when it looked as if there might be a default on Nakheel bonds. Both emirates have learnt from that PR disaster and relations between the two have seldom been on a better footing.

UAE unity rules

Rather than disunite the United Arab Emirates there has been a new awareness of collectice self-interest, or to be more frank a realisation that Dubai and Abu Dhabi sink or swim together.

How difficult then is the task that lies ahead? Dubai raised a $1.25 billion bond on international markets at the end of September, and both Emaar Properties and Dubai Electricity and Water have also raised money in bond markets.

But then let us not forget the financial position of Abu Dhabi, arguably the world’s richest city. There is $450-650 billion in its sovereign wealth funds; $3-4 trillion worth of oil in the ground which makes the average family worth $100 million plus; and the cash flow from the rising oil price.

The anomaly was surely that Dubai and Abu Dhabi used to operate entirely without debt in the past, simply using oil revenues and retained business profits to fund investments in infrastructure. Both cities could have grown even faster by borrowing and took a very conservative approach.

More Abu Dhabi bond issues

To refinance the UAE is surely not really a problem with all that wealth to hand. Abu Dhabi needs to issue bonds to recapitalize the debts. That is what happened in the Dubai debt crisis a year ago.

But as analysts point out there will always be strings attached, and clearly Dubai would like to keep as much as it can. However, there may come a tipping point when it is obvious that the objective of getting the show back on the road quickly supercedes a longer term outlook, or indeed becomes imperative to secure the long-term.

The upcoming $42.3 billion in short-term debt will surely focus attention, as has the alleged $2.7 billion funding gap has at Aldar Properties. For wiping the slate clean after the recent boom would be in the interest of all parties, and it will happen sooner or later.

Ironically while Bank of America Merrill Lynch has highlighted Aldar’s problems, the bank itself is the subject of intense speculation about the viability of its own balance sheet (click here). These are still difficult times for financial markets and only the players with the strongest financial backing will ultimately survive.

Posted on 08 November 2010

Du Quarterly Profit More than Doubles on New Subscribers, Beats Estimates - Bloomberg

Emirates Integrated Telecommunications Co., the United Arab Emirates’ second-biggest phone company, said third-quarter profit more than doubled, beating estimates, as its client base grew.

Net income climbed to 163.1 million dirhams ($44 million) from 78.55 million dirhams a year earlier, the company known as Du said in a statement to the Dubai bourse today. The median estimate of six analysts was for a profit of 139.5 million dirhams, according to data compiled by Bloomberg. Revenue increased 31 percent to 1.7 billion dirhams.

“By the end of August we had an estimated 37 percent market share of active mobile subscribers and expect this to have increased further by the end of the quarter, which is an outstanding achievement in just three years,” Chief Executive Officer Osman Sultan said in the statement. “We will continue to lead the way for fixed and mobile broadband services.”

Net income climbed to 163.1 million dirhams ($44 million) from 78.55 million dirhams a year earlier, the company known as Du said in a statement to the Dubai bourse today. The median estimate of six analysts was for a profit of 139.5 million dirhams, according to data compiled by Bloomberg. Revenue increased 31 percent to 1.7 billion dirhams.

“By the end of August we had an estimated 37 percent market share of active mobile subscribers and expect this to have increased further by the end of the quarter, which is an outstanding achievement in just three years,” Chief Executive Officer Osman Sultan said in the statement. “We will continue to lead the way for fixed and mobile broadband services.”

Qatar to widen civil dispute net

Qatar is making a bold move into the regional legal scene with its own specialist court for civil disputes. The Qatar Financial Centre (QFC) Judiciary is busy building its first court room in a tower in the capital, due to be finished next month.

Judges on the new court roster include: Lord Woolf, formerly the lord chief justice of England and Wales; Lord Cullen, formerly the lord justice general and the lord president of the court of session in Scotland; and Justice Aziz Ahmadi, formerly the chief justice of India.

But unlike its peer in the UAE, which has the most established track record for cases in the Gulf, the QFC Judiciary hopes to become a dispute resolution centre for companies not necessarily based in Qatar. "A key difference for us is our jurisdiction," said Robert Musgrove, the recently appointed chief executive of the Qatar Civil and Commercial Court. Mr Musgrove was previously the head of the civil justice council for England and Wales.

Judges on the new court roster include: Lord Woolf, formerly the lord chief justice of England and Wales; Lord Cullen, formerly the lord justice general and the lord president of the court of session in Scotland; and Justice Aziz Ahmadi, formerly the chief justice of India.

But unlike its peer in the UAE, which has the most established track record for cases in the Gulf, the QFC Judiciary hopes to become a dispute resolution centre for companies not necessarily based in Qatar. "A key difference for us is our jurisdiction," said Robert Musgrove, the recently appointed chief executive of the Qatar Civil and Commercial Court. Mr Musgrove was previously the head of the civil justice council for England and Wales.

DP World back to markets

DP World, the ports and logistics company owned by the Government-related Dubai World, plans to return to the international capital markets for up to US$3.25 billion (Dh11.93bn) of debt financing, probably next year.

The company announced its intentions in an updated prospectus filed with the London Stock Exchange, where it is planning a listing for next spring.

The move signals a renewed appetite from Dubai companies to access the debt markets after the successful conclusion of negotiations for the restructuring of $24.9bn of debt by Dubai World, the property and transport conglomerate.

The company announced its intentions in an updated prospectus filed with the London Stock Exchange, where it is planning a listing for next spring.

The move signals a renewed appetite from Dubai companies to access the debt markets after the successful conclusion of negotiations for the restructuring of $24.9bn of debt by Dubai World, the property and transport conglomerate.

Hope and fear over Dubai debt

DP World's reawakened interest in the international capital markets signals another step in the recovery of Dubai Inc, but the emirate still faces uncertainties over how it will refinance a significant amount of debt coming due over the next two years.

Dubai's debt situation has been under the microscope since Dubai World, one of the emirate's biggest conglomerates, sought a standstill on debt repayments almost a year ago. Initial fears of a sovereign default proved unfounded, and the ensuing European debt crisis soon stole the spotlight.

But Dubai has remained under scrutiny because of the sheer size of its total debt, estimated at US$109 billion (Dh400.3bn) by the IMF in February.

Dubai's debt situation has been under the microscope since Dubai World, one of the emirate's biggest conglomerates, sought a standstill on debt repayments almost a year ago. Initial fears of a sovereign default proved unfounded, and the ensuing European debt crisis soon stole the spotlight.

But Dubai has remained under scrutiny because of the sheer size of its total debt, estimated at US$109 billion (Dh400.3bn) by the IMF in February.

Sukuk market will bounce back over the next two years - Arab News

ELAF Bank is a wholesale Islamic bank incorporated in Bahrain in 2007. Its shareholders include Aref Investment Group of Kuwait; Kuwait Investment Company (KIC); Sukuk Holding Company; Islamic Corporation for the Development of the Private Sector (ICD), the private sector funding arm of the Islamic Development Bank; and Qatar Islamic Bank.

It started with the original objective of developing a secondary market in sukuk and to be a market maker. In fact its original name was the cumbersome Sukuk Exchange Central Bank. But the oncoming global financial crisis forced the bank to retreat into more vanilla investment banking to generate enough income to cover its expenses and to prepare for the recovery in the market in 2010-2011.

The CEO of Elaf Bank is Jamil El-Jaroudi, a seasoned Islamic banker who previously worked for Shamil Bank of Bahrain, then a subsidiary of the Dar Al-Maal Al-Islami (DMI) Group, and subsequently worked as CEO of Arab Finance House in Lebanon. Here El-Jaroudi discusses with Mushtak Parker the latest developments at Elaf Bank, the state of the sukuk market and why he is optimistic about the future of the Islamic banking industry.

It started with the original objective of developing a secondary market in sukuk and to be a market maker. In fact its original name was the cumbersome Sukuk Exchange Central Bank. But the oncoming global financial crisis forced the bank to retreat into more vanilla investment banking to generate enough income to cover its expenses and to prepare for the recovery in the market in 2010-2011.

The CEO of Elaf Bank is Jamil El-Jaroudi, a seasoned Islamic banker who previously worked for Shamil Bank of Bahrain, then a subsidiary of the Dar Al-Maal Al-Islami (DMI) Group, and subsequently worked as CEO of Arab Finance House in Lebanon. Here El-Jaroudi discusses with Mushtak Parker the latest developments at Elaf Bank, the state of the sukuk market and why he is optimistic about the future of the Islamic banking industry.

WAM | GCC monetary Union is not possible without UAE : Al Attiyah

As the second largest Gulf economy, the UAE is a basic element in the GCC Monetary Union and Single Currency, the GCC chief affirmed today.

''The Gulf Monetary Union will not come to life without the UAE,'' Secretary-General of GCC Abdul Rahaman bin Hamad Attiyah said on the sideline a seminar on 'Gulf Common Market: From Cooperation to Integration', hosted by the Ministry of Finance in Dubai.

Al Attiyah hoped the UAE would reconsider its position on joining the Gulf Monetary Union.

''The Gulf Monetary Union will not come to life without the UAE,'' Secretary-General of GCC Abdul Rahaman bin Hamad Attiyah said on the sideline a seminar on 'Gulf Common Market: From Cooperation to Integration', hosted by the Ministry of Finance in Dubai.

Al Attiyah hoped the UAE would reconsider its position on joining the Gulf Monetary Union.

Subscribe to:

Comments (Atom)