In Putin’s Russia, risk prices you | FT Alphaville:

Or, why investors might be less than sanguine about sanctions against Russia.

We could start with the OFZs.

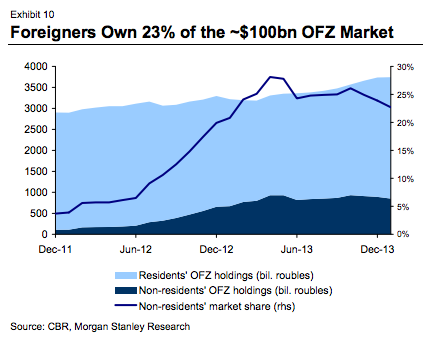

(Morgan Stanley’s chart — click to enlarge)

Just how is it that foreigners have come to own over a fifth ($20bn) of Russia’s domestic government bond market, after all?

Well, because of painstaking efforts to connect Russia back to the basic plumbing of international finance over the years, actually. At least in part.

The impressive quadrupling of non-resident share in a year which you can see from the middle of 2012, for example — that’s the boost after Euroclear and Clearstream said they would start clearing OFZs within their systems. It’s kind of the bond-market equivalent of visa-free travel: a big deal. Elsewhere Russian bonds have also risen to 10 per cent of the GBI, the main artery of emerging-market bond indices.

In other words, it’s important to note at the start of a post like this that there was a genuine rehabilitation of Russia as a place to get money in, and as importantly, out, in recent years. It makes it all very ironic now.

After all, between the prospect of “phase three” financial sanctions by the US and EU if events escalate in the annexation of Crimea, and the potential for capital controls from the Russian side — the plumbing is being placed in danger all over again. In part, tellingly, this is through markets anticipating the authorities’ worst-case options.

The risk repricing

It’s interesting this isn’t being noticed more. Repricing of this risk will do very real damage, even if far from crippling, to the Russian economy (which is already poorly).

Of course, this concept cuts across some of the blather of recent weeks — that the Putinist Kremlin is filled with geopolitical geniuses, and/or that western politicians arevalets of the oligarchs. (That argument must have appealed to many because, if the City looked too big to risk a Russian exodus, then it supported the view that the City is too big anyway. It was still wrong.)

The risk can already be seen quite granularly in the FX market. One-year non-deliverable forwards for the rouble/dollar rate last week began trading at a rare premium to their onshore deliverable counterparts. The clue’s in the name. Foreign holders of the latter are starting to wonder if they’ll be able to take delivery of spot roubles a year out.

But it also speaks to a much broader issue with investing in Russia. Since Mr Putin became president in 2000, around $350bn of private-sector capital has flowed out of the country, according to Morgan Stanley — into Belgravia property, Cypriot brass-plates, what have you. The sloshing around of this wealth has been seen as a weakness of the west (see: oligarchs, valets).

Even so, it also means foreign investors should have been aware they were putting money into relatively hollowed-out Russian bond and equity markets. The locals’ assets weren’t sticking around much.

This somewhat belies the idea of Russia overall having an autarkic, oil-exporting balance sheet — although that’s perfectly real. Half a trillion dollars in FX reserves (less than half of that in US-dollar securities, which could in theory become difficult to access). A balanced budget (well, the Kremlin will need it, if it’s going to dispense imperial largesse to Crimea now). Government external debt to GDP is in single digits. The entire economy is a giant oil-price proxy. Sanctions can’t cripple Russia at all then, that’s true. Especially energy sanctions.

Then again, what would financial sanctions — of long duration and unprecedented complexity — mean to investors only just through that recent rehabilitation of Russia?

Sanctions complexity

It is true that complexity would be a challenge for the sanctions-setters themselves.

If Russian officials planning the invasion of another country have been anywhere near as careful about executing offshore financial escape-hatches as their compatriots can be in divorce cases before English courts… it will be complicated for the west’s asset-freezing agencies to track, even at the level of targeted sanctions against individuals.

At the next level of sanctions — directions to avoid business with named institutions — it is legally more complicated still. Partly this is because of the international co-ordination necessary (which might not even help that much).

Partly it is because these institutions could sue right back. Bank Mellat is a name we’ve been surprised to have not heard much. Only recently, Iran’s largest private bank quashed both UK sanctions under the Counter-Terrorism Act, and an overlapping EU asset freeze. In the former, the UK Supreme Court found late last year that the UK order was “irrational in its incidence and disproportionate to any contribution which it could rationally be expected to make to its objective.”

On the other hand, an institution like the US Office of Foreign Assets Control arguably thrives on the complexity and ambiguity of sanctions regimes, as it has with Iran. Its remit is wide-ranging and extra-territorial: financial institutions have to self-report their compliance with OFAC strictures. (The story of Argentina’s pari passu saga is — no joke — partly the story of US courts establishing their own highly effective sanctions regime against a recalcitrant actor.)

And that, probably is where investors with their OFZ holdings and index weightings may start to feel like sitting ducks. (Another, more US-focused Morgan Stanley chart – click to enlarge)

Russia vs Iran

Sanctions are wasting assets. They probably become less effective over time, which is why governments take their sweet time threatening them instead first, and also establish gradations of severity in order to signal the willingness to lop off bits of their own financial systems to compel a transgressor.

But the economic backdrop to sanctions, if they do go all the way on Russia, would be very different even to that facing Iran over its nuclear programme, for example. Sanctions here had a deleterious impact on oil exports (they may also have worked, in compelling Tehran to talk). But ultimately they’re fingers in the dyke.

Money would probably love to flow in to Iran, in the long run. Imagine Turkey with a current account surplus and a tenth of world oil reserves, plus a stock market with $170bn in capitalisation already, as Renaissance Capital put it in an excellent note last week. The Iranian economy arguably shouldn’t still even be a frontier market, on its fundamentals, though politically it remains far off frontier.

Perhaps Russia, however, never stopped being a frontier market: investors just pretended otherwise. The Moscow stock market has a $500bn capitalisation, sure, and London creaks under the listings and GDRs of Russian corporate names. Frontier appellation seems absurd.

But the whiff of sanctions grapeshot will just remind investors of deep-seated anxieties about the safety of keeping money in Russia, or investing in companies which do. Their reaction will get reflected in turn in the rates that are charged Russian corporate borrowers, and even the stance of the central bank, in defending the rouble. That’s a pity, because there are plenty of decent Russian companies (many of which would be helped by a weakening rouble). Sadly, Putin risk is wrecking them.

Same for some western companies. It will certainly suck to be BP if this environment persists, for example, with its over-dependence on Russia for production growth. But if anyone is still wondering why there are Russian companies which can trade just four or five times their forward earnings (Gazprom itself is not far off two times)… stop. The answer was always there. The sanctions stuff may just show it was the right one.

'via Blog this'

No comments:

Post a Comment