From Reuters today:

Russia’s economy is stagnating as data showed on Wednesday that capital worth $75 billion has left the country so far this year following sanctions on Moscow over its involvement in Ukraine.

“We have for now a period of stagnation, or a pause in growth,” Deputy Economy Minister Andrei Klepach was quoted as saying in an interview where he also said that GDP was flat from April to June after shrinking 0.5 percent in the first quarter.

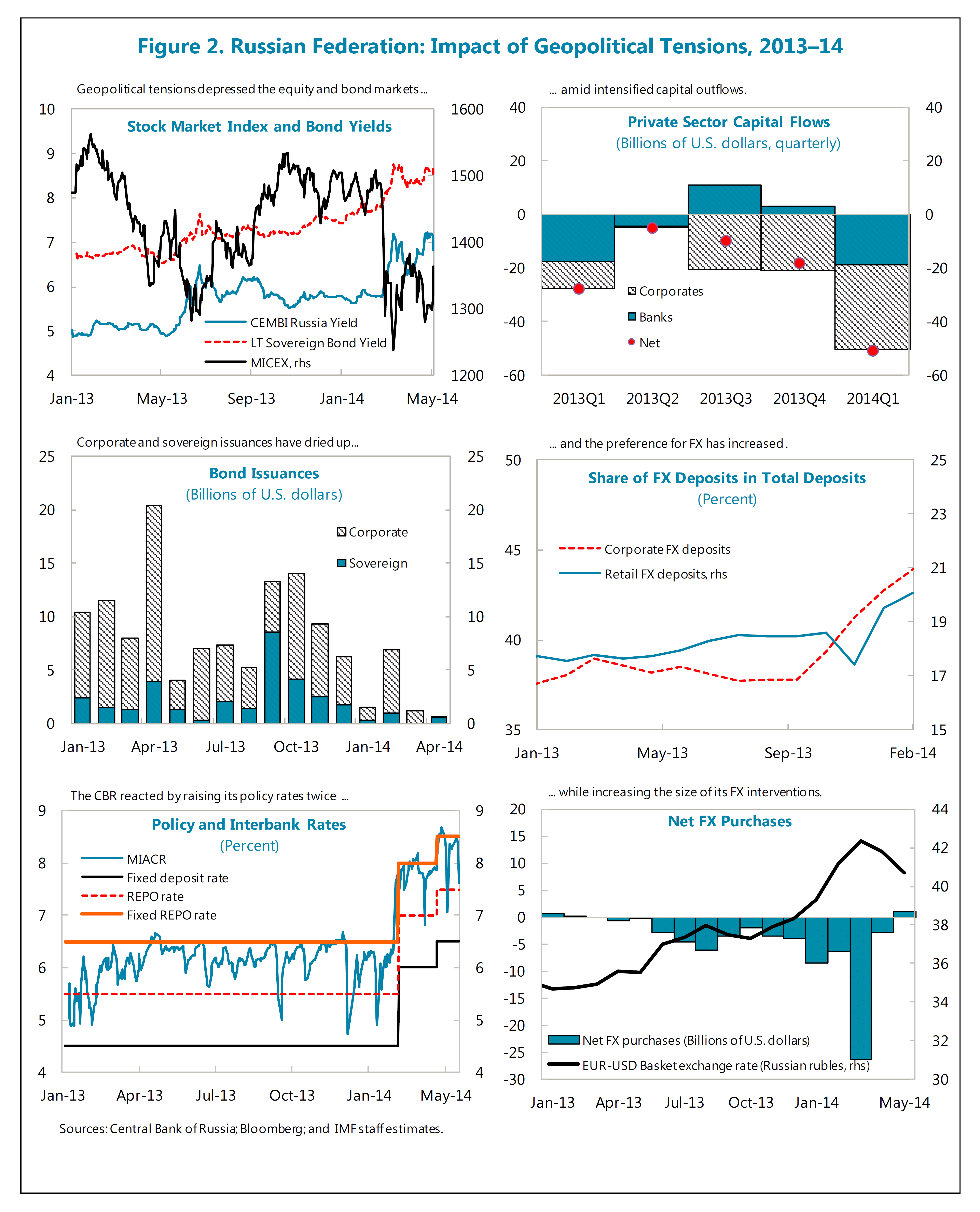

Here are some indicators of stress from political uncertainty, from the IMF’s recent Article IV report on the Russian Federation.

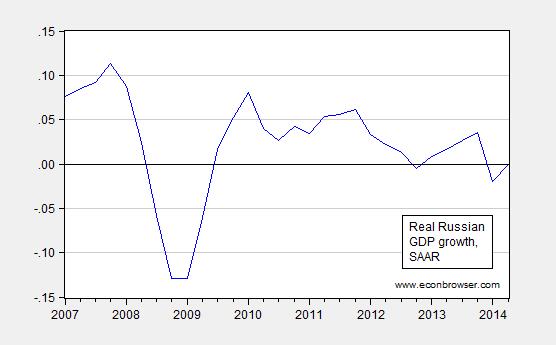

And here is an updated version of GDP growth.

Figure 1: Russian q/q annualized GDP growth, in 2000 prices. Source: OECD via FRED through 2013Q4, Reuters for 2014, and author’s calculations.

From the report:

Net private capital outflows increased significantly in the first quarter of 2014 to US$51 billion (Figure 2 and Box 3). Reserves at the CBR experienced additional downward pressures following the sharp increase in FX intervention in early March. The increased level of FX swaps and correspondent accounts between the CBR and domestic banks has temporarily cushioned the level of reserves, which have not declined by the total amount of interventions. While FX swaps were used to access CBR liquidity, the increase in the level of correspondent accounts at the CBR has reflected increased foreign assets repatriation by domestic banks amidst increasing geopolitical uncertainties.Geopolitical tensions are negatively weighing on the cost and access to financing. Since March, sovereign and private issuances have declined very sharply, with borrowing rates increasing by an average of 100–150 basis points (Figure 2). The government has also cancelled a number of domestic auctions. Moody’s and Fitch revised the outlook on Russia’s sovereign BBB rating from stable to negative while S&P downgraded the sovereign rating by one notch to BBB-, its lowest investment grade category. This downgrade forced similar ratings cut on major Russian corporations such as Gazprom, Rosneft, and VTB bank, as well as subsidiaries of international banks. The geopolitical uncertainty has also given rise to dollarization pressures.

The outflow of $75 billion means that $24 billion worth of capital left Russia (on net) in the second quarter. While this means the pace of outflows is declining, it also means that the first half of the year witnessed a greater outflow than in the entirety of 2013. For certain, Russia seems on the way to the $100 billion outflow for 2014 that some had warned of.

How much of this outflow, and hence weakness in growth, is due to the imposition of sanctions, or the uncertainty associated with the possibility of additional sanctions? FromReuters:

Deputy Finance Minister Sergei Storchak said on Tuesday that sanctions were having a serious indirect impact” and warned of retaliation against further measures by the West.…“The real damage to the economy is potentially much more serious and comes from the voluntary self-sanctions taken by foreign investors, credit providers and some foreign companies active in Russia,” Chris Weafer, a partner of Macro-Advisory, a consulting firm in Moscow, said in a note published by the European Leadership Network.“While not compelled legally to restrict activities in Russia it is clear that many investors and big international companies have suspended new deals in Russia and have cut risk exposure.”

In other words, the impact has been greater than some skeptics have asserted, and perhaps more in line with my earlier views. [1]

This piece is cross-posted from Econbrowser with permission.

'via Blog this'

No comments:

Post a Comment