Wednesday, 23 December 2009

Revealed: Opec’s fears that rich countries’ appetite for oil is waning

The Opec oil cartel has repeated it through the year: as a contribution to the global economy recovery, it was supporting moderate oil prices.

Saudi Arabia put numbers on the cartel’s words, describing the $70-$80 a barrel range as “excellent”.

For sure, Opec’s aim of $70-$80 a barrel – the group avoid talking about a target – has helped the global economy, particularly of poor oil importing countries.

But there are signs that the oil cartel is not as altruistic at it appears at first glance. Opec appears to be as concerned about the global economy as to drive consumers away from oil.It is the clearest recognition yet that high oil prices could damage the cartel’s interest in the long-term by reducing for ever energy demand.

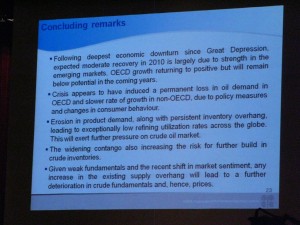

The deliberation came to the light as Opec – it appears that by mistake on the chaos surrounding the meeting in Luanda, Angola’s capital – allowed reporters to remain in the plenary room while the group’s economist told ministers their latest findings. “Crisis appears to have induced a permanent loss in oil demand in OECD and slower rate of growth in non-OECD, due to policy measures and changes in consumer behaviour,” the “concluding remarks” of the presentation read.

The Energy Source blog had in Luanda a still camera at hand – so we took a picture of the power point slide for the record.

For Opec standards, the warning is pretty heavy stuff. In plain language, it means that it acknowledges that governments’ measures to save fossil fuels – a move to biofuels, but also to nuclear, wind, solar and other renewable energy sources – and consumers attitude – read, for example, buying smaller cars or moving into public transport – are hurting, Although the cartel pointed to the generic “crisis” as the reason of the permanent loss in demand, the changes it described – government policy and consumer’s behaviour – are not the result of the financial crisis, but of the oil prices crisis of 2008.

The cartel’s presentation did not say how much oil demand has being loss or destructed, but it is clear from the presentation that the figure has to be large or, on the contrary, the group’s economist will have not highlighted it. The presentation’s warning appears to back the view of some critics of Opec’s policy of high oil prices between 2006 and 2008, when oil prices peaked at $147 a barrel.

Sheik Yamani, the former oil minister from Saudi Arabia, was among them, repeating his famous – albeit cliché nowadays – warning: the age of stone did not end because a shortage of stones, neither the oil age will end because a lack of oil. On the contrary, the sheik argued last year, plenty of oil will be left underground because high prices will drive consumers away for oil, cutting for ever demand. There are examples in the past: demand in Western Europe has yet to recover to the level it reached in the mid-1970s, before the explosion in prices of the second oil crisis. Neither has Japan’s demand surged back to the levels of early 1980s.

Now, it appears that the demand of the US peaked around 2005. The International Energy Agency, the western countries’ oil watchdog, says that its “working assumption remains that a degree of structural demand destruction has occurred, notably in the OECD, which may constrain overall levels of demand growth in future.”

The IEA says that the oil intensity – a measure of how much oil is necessary to consume for each unit of GDP – declined by about 2.2 per cent between 1998-2008 worldwide, but anticipates an acceleration to 3 per cent over 2011-2014.

Iraq oil auctions cause concerns over stability in Gulf hierarchy

Iraq looks set to shake up the Middle East's oil hierarchy after the Iraqi Oil Ministry ended its second bidding round last week, awarding seven oilfields in a tender which could eventually increase the war-torn country's capacity to 12 million barrels per day.

The auction, which centered on oilfields ready for development, saw Russian and Chinese oil firms secure lucrative contracts at the expense of companies from the United States who were largely absent from the tender for deals to tap Iraqi oil reserves, the world's third-largest.

While the lack of success for US companies caused some surprise - considering the widespread belief that the US-led invasion was based on a thirst for oil - the main topic of debate after the auction was the likelihood that Iraq's new oil power would move Baghdad into the big league of oil producing countries and give it a strong hand in future Organization of Petroleum Exporting Countries (OPEC) negotiations on output quotas.

The auction, which centered on oilfields ready for development, saw Russian and Chinese oil firms secure lucrative contracts at the expense of companies from the United States who were largely absent from the tender for deals to tap Iraqi oil reserves, the world's third-largest.

While the lack of success for US companies caused some surprise - considering the widespread belief that the US-led invasion was based on a thirst for oil - the main topic of debate after the auction was the likelihood that Iraq's new oil power would move Baghdad into the big league of oil producing countries and give it a strong hand in future Organization of Petroleum Exporting Countries (OPEC) negotiations on output quotas.

Dubai Shares Fall Most in World as Investors Wait for Debt Plan

Dubai stocks retreated the most in two weeks as investors waited for state-owned holding company Dubai World to present a debt restructuring plan.

Emirates NBD PJSC, a Dubai-government controlled lender, tumbled to its lowest level in seven months. Emaar Properties PJSC, the United Arab Emirates’ biggest construction company, fell for a second day. The DFM General Index dropped 3.8 percent, the biggest fluctuations among 89 indexes tracked globally by Bloomberg News, to 1,734.65 at 1:07 p.m. in Dubai. Dubai’s benchmark index has gained 6 percent this year.

Dubai World may present a “standstill” offer to banks in early January as it aims to restructure $22 billion of debt, said three bankers who attended a presentation on the matter earlier this week. The company told lenders it needs time to allow its assets to recover from a drop in value following the credit crunch, said the bankers, who declined to be identified because the meeting was private.

Emirates NBD PJSC, a Dubai-government controlled lender, tumbled to its lowest level in seven months. Emaar Properties PJSC, the United Arab Emirates’ biggest construction company, fell for a second day. The DFM General Index dropped 3.8 percent, the biggest fluctuations among 89 indexes tracked globally by Bloomberg News, to 1,734.65 at 1:07 p.m. in Dubai. Dubai’s benchmark index has gained 6 percent this year.

Dubai World may present a “standstill” offer to banks in early January as it aims to restructure $22 billion of debt, said three bankers who attended a presentation on the matter earlier this week. The company told lenders it needs time to allow its assets to recover from a drop in value following the credit crunch, said the bankers, who declined to be identified because the meeting was private.

Fitch Affirms Bahrain's Sovereign Rating

Fitch Ratings affirmed Bahrain's Long-term foreign and local currency Issuer Default Ratings at 'A' and 'A+' respectively. The Outlook on the Long-term IDR remained stable. The rating agency also affirmed short-term foreign currency IDR at 'F1' and Country Ceiling at 'A+'.

Purvi Harlalka, Associate Director in Fitch's Sovereign group said, "Although growth has slowed and the budget has moved into large deficit, government and external debt ratios will remain better than rated peers. Domestic banks' exposure to the property sector will continue to exert pressure on asset quality, but Fitch believes further deterioration can be absorbed with capital ratios remaining adequate, supporting the Stable Outlook."

Purvi Harlalka, Associate Director in Fitch's Sovereign group said, "Although growth has slowed and the budget has moved into large deficit, government and external debt ratios will remain better than rated peers. Domestic banks' exposure to the property sector will continue to exert pressure on asset quality, but Fitch believes further deterioration can be absorbed with capital ratios remaining adequate, supporting the Stable Outlook."

Why is the DFM buying Nasdaq Dubai?

Following yesterday’s surprise announcement that the Dubai Financial Market is to acquire 100 per cent of Nasdaq Dubai there some unanswered questions.

For a start, who is selling Nasdaq Dubai? Nasdaq Dubai is one-third owned by Nasdaq OMX and two thirds by Bourse Dubai. Details of the deal show that the DFM will pay $120 million in cash and $20 million in its own shares to Bourse Dubai to take control of Nasdaq Dubai; and Nasdaq OMX will take a one per cent stake in the DFM.

And who owns Bourse Dubai? The Dubai Government, which also owns an 80 per cent stake in the DFM. So as a result of the deal the Dubai Government will slightly increase its stake in the DFM and pick up $102 million.

For a start, who is selling Nasdaq Dubai? Nasdaq Dubai is one-third owned by Nasdaq OMX and two thirds by Bourse Dubai. Details of the deal show that the DFM will pay $120 million in cash and $20 million in its own shares to Bourse Dubai to take control of Nasdaq Dubai; and Nasdaq OMX will take a one per cent stake in the DFM.

And who owns Bourse Dubai? The Dubai Government, which also owns an 80 per cent stake in the DFM. So as a result of the deal the Dubai Government will slightly increase its stake in the DFM and pick up $102 million.

Gulf News Urges Reporters To Tone Down Dubai Debt Coverage

By Maria Abi-Habib Of ZAWYA DOW JONES DUBAI (Zawya Dow Jones)--Gulf News, a newspaper part-owned by a senior government minister in the United Arab Emirates, has told its journalists to avoid using the words "bailout" and "default" when writing about Dubai's debt crisis, according to an internal memo sent to staff and seen by Zawya Dow Jones. Reporters for the paper, the largest English-language daily in the U.A.E., were also urged to steer clear of the phrase "debt crisis" and asked to "ensure the following politically correct terminology is used" - words such as "financial consolidation" and "fiscal support" - when describing the sheikdom's economic problems and the assistance it has received from Abu Dhabi, according to the note sent Dec. 14.

"This is a style guide," said Francis Matthew, the Dubai-based paper's editor-at-large when asked by Zawya Dow Jones about the memo. "We're trying to restrict people from using financially incorrect terms." U.A.E. officials have criticized international press coverage of Dubai's debt crisis since the emirate surprised markets on Nov.

25, saying it needed to freeze $26 billion of debt owed by one of its largest government-owned groups, Dubai World. Abu Dhabi bailed out Dubai on Dec. 14 with $10 billion, which the government used partly to pay off an Islamic bond due on that day.

Dubai's finance chief, Abdulrahman Al Saleh, this month blamed the media for spreading "blind panic" about the emirate's financial woes following the standstill request that triggered a downgrade of many of its banks and government-owned companies. The sheikdom, which closely monitors the media, has come under intense scrutiny as it struggles to contain the estimated $80 billion of debt, mostly racked up by its government-owned companies building speculative real estate and infrastructure projects. The Sunday Times was ordered off shelves in the U.A.E.

on Nov. 29 after the paper carried a double-page graphic illustrating Dubai's ruler, Sheik Mohammed bin Rashid al Maktoum, sinking in a sea of debt. Its sister publication, The Times, was censored in the U.A.E.

on Dec. 5 for a story that described Sheik Mohammed as a "benign dictator" and criticized his management of the economy. The Sunday Times and The Times are part of News International, a unit of News Corp., owner of Dow Jones & Co, publisher of this newswire.

Gulf News is published by Al Nisr Publishing, which is part-owned by the country's Minister of State for Financial Affairs, Obaid Humaid Al Tayer, who chairs the company. Abdulrahman Hassan Abdulhamid Al Rostamani and Jumaa Al Majid, two large merchant families in Dubai, are also part owners along with the Al Tayer Group, according to Zawya.com's corporate monitor service. -By Maria Abi-Habib, Dow Jones Newswires; +97150-941 9737; maria.habib@dowjones.com Copyright (c) 2009 Dow Jones & Co.

(END) Dow Jones Newswires December 23, 2009 00:01 ET (05:01 GMT)END

"This is a style guide," said Francis Matthew, the Dubai-based paper's editor-at-large when asked by Zawya Dow Jones about the memo. "We're trying to restrict people from using financially incorrect terms." U.A.E. officials have criticized international press coverage of Dubai's debt crisis since the emirate surprised markets on Nov.

25, saying it needed to freeze $26 billion of debt owed by one of its largest government-owned groups, Dubai World. Abu Dhabi bailed out Dubai on Dec. 14 with $10 billion, which the government used partly to pay off an Islamic bond due on that day.

Dubai's finance chief, Abdulrahman Al Saleh, this month blamed the media for spreading "blind panic" about the emirate's financial woes following the standstill request that triggered a downgrade of many of its banks and government-owned companies. The sheikdom, which closely monitors the media, has come under intense scrutiny as it struggles to contain the estimated $80 billion of debt, mostly racked up by its government-owned companies building speculative real estate and infrastructure projects. The Sunday Times was ordered off shelves in the U.A.E.

on Nov. 29 after the paper carried a double-page graphic illustrating Dubai's ruler, Sheik Mohammed bin Rashid al Maktoum, sinking in a sea of debt. Its sister publication, The Times, was censored in the U.A.E.

on Dec. 5 for a story that described Sheik Mohammed as a "benign dictator" and criticized his management of the economy. The Sunday Times and The Times are part of News International, a unit of News Corp., owner of Dow Jones & Co, publisher of this newswire.

Gulf News is published by Al Nisr Publishing, which is part-owned by the country's Minister of State for Financial Affairs, Obaid Humaid Al Tayer, who chairs the company. Abdulrahman Hassan Abdulhamid Al Rostamani and Jumaa Al Majid, two large merchant families in Dubai, are also part owners along with the Al Tayer Group, according to Zawya.com's corporate monitor service. -By Maria Abi-Habib, Dow Jones Newswires; +97150-941 9737; maria.habib@dowjones.com Copyright (c) 2009 Dow Jones & Co.

(END) Dow Jones Newswires December 23, 2009 00:01 ET (05:01 GMT)END

Wealth fund assets recover ground

The value of assets managed by Abu Dhabi’s two leading sovereign wealth funds is likely to have risen to US$425 billion (Dh1.55 trillion) after this year’s rally in oil prices and global financial markets, estimates by an economic consultancy show.

Rachel Ziemba, an economist at RGE Monitor in New York, said the combined assets of the Abu Dhabi Investment Authority (ADIA) and the Abu Dhabi Investment Council (ADIC) had probably recovered by as much as 20 per cent after major losses from the global financial crisis.

“That implies quite a strong revaluation of the portfolio since February when I estimated AUM [assets under management] was closer to $300bn,” Ms Ziemba said.

Rachel Ziemba, an economist at RGE Monitor in New York, said the combined assets of the Abu Dhabi Investment Authority (ADIA) and the Abu Dhabi Investment Council (ADIC) had probably recovered by as much as 20 per cent after major losses from the global financial crisis.

“That implies quite a strong revaluation of the portfolio since February when I estimated AUM [assets under management] was closer to $300bn,” Ms Ziemba said.

As Dubai World turns, question is not how but when

The first formal meeting between Dubai World and its 90-plus creditors passed off as something of an anticlimax, but it was always going to be so.

There was never the remotest possibility that Aidan Birkett, the company’s chief restructuring officer who is now calling the shots on strategy, was going to be pictured beaming with a group of international bankers, waving a piece of paper Chamberlain-style and proclaiming “solvency in our time” for those parts of Dubai World put up for restructuring.

Bankers who attended the meeting said it was “businesslike” and useful as a first move in trying to get their cash back. For their part, there was never any possibility they would emerge with sacks of cash handed over by Mr Birkett at the Dubai World Trade Centre.

There was never the remotest possibility that Aidan Birkett, the company’s chief restructuring officer who is now calling the shots on strategy, was going to be pictured beaming with a group of international bankers, waving a piece of paper Chamberlain-style and proclaiming “solvency in our time” for those parts of Dubai World put up for restructuring.

Bankers who attended the meeting said it was “businesslike” and useful as a first move in trying to get their cash back. For their part, there was never any possibility they would emerge with sacks of cash handed over by Mr Birkett at the Dubai World Trade Centre.

Dubai World will get government financial support

State-owned conglomerate Dubai World said the Government will provide financial support to cover its working capital expenses.

"As long as a standstill is successfully implemented, Dubai World has assurances that the Government of Dubai, through the DFSF, will provide financial support to cover working capital and interest expenses to ensure the continuity of key projects," an statement from Dubai World said.

The DFSF, Dubai Financial Support Fund, has been set up to manage the money being used to pay off the emirate's debt.

"As long as a standstill is successfully implemented, Dubai World has assurances that the Government of Dubai, through the DFSF, will provide financial support to cover working capital and interest expenses to ensure the continuity of key projects," an statement from Dubai World said.

The DFSF, Dubai Financial Support Fund, has been set up to manage the money being used to pay off the emirate's debt.

Dubai Real Estate and Its Connection to the U.S

If you've been to one of my presentations either in person or through a virtual classroom, you know that I refer to our Dubai center and the massive amount of real estate available there. So with Dubai in the headlines for the last month, I thought I'd take the opportunity to look a little closer at Dubai's real estate market and their investments in the U.S.

Here's a short history lesson on Dubai, known as the home of sand, sun and shopping. A century ago, it was a peaceful town where Bedouin traders and pearl divers lodged. Today those merchants are gone. The city stands with its futuristic skyscrapers, alongside mosques, as one of the greatest cities in the world. Dubai boasts of its tremendous development at a pace unparalleled anywhere in the world. If you look into the ancient history of the region, there are suggestions that humans have been living there since at least 3000 BC. What a dramatic change!

Dubai has a prime location between the Mediterranean and the Indian Ocean. These trade routes have been exceptionally valuable for much of this area's history. By the late 16th century, the Portuguese controlled local trade routes. This pushed the tribes that had lived on the land to oases, far from the coast. The British gained control of the region's waterways in 1766. Dubai was amidst local power struggles and European Imperialism. In 1833, the Bani Yas (a neighboring tribal power), under the leadership of Maktoum bin Butti, raided Dubai and took the area. The Al-Maktoum family still rules the emirate today. In 1971, Dubai became the seventh emirate of the newly formed UAE. Dubai's story is amazing, as one writer put it, "A rags-to-riches tale."

Here's a short history lesson on Dubai, known as the home of sand, sun and shopping. A century ago, it was a peaceful town where Bedouin traders and pearl divers lodged. Today those merchants are gone. The city stands with its futuristic skyscrapers, alongside mosques, as one of the greatest cities in the world. Dubai boasts of its tremendous development at a pace unparalleled anywhere in the world. If you look into the ancient history of the region, there are suggestions that humans have been living there since at least 3000 BC. What a dramatic change!

Dubai has a prime location between the Mediterranean and the Indian Ocean. These trade routes have been exceptionally valuable for much of this area's history. By the late 16th century, the Portuguese controlled local trade routes. This pushed the tribes that had lived on the land to oases, far from the coast. The British gained control of the region's waterways in 1766. Dubai was amidst local power struggles and European Imperialism. In 1833, the Bani Yas (a neighboring tribal power), under the leadership of Maktoum bin Butti, raided Dubai and took the area. The Al-Maktoum family still rules the emirate today. In 1971, Dubai became the seventh emirate of the newly formed UAE. Dubai's story is amazing, as one writer put it, "A rags-to-riches tale."

Dubai exchange tie-up teaches a hard truth

Nasdaq Dubai, which was set up in 2005 and boasts just three primary equity listings, is being acquired by its larger local rival, Dubai Financial Market (DFM).

The move consolidates the government ownership of Dubai's exchanges. US operator Nasdaq OMX will swap its 33.3pc stake in the international exchange for a 1pc stake - worth $39m (£24m0 based on Monday's closing price - in DFM. That would leave Nasdaq OMX facing a 70pc write-down on the current book value of its 2008 investment.

For now, the deal won't change the way the exchanges do business. They will continue to operate as separate entities which share back office functions. Over time, though, a full operational merger is probable, once some kinks - in trading currencies, regulatory standards and procedures - are ironed out.

The move consolidates the government ownership of Dubai's exchanges. US operator Nasdaq OMX will swap its 33.3pc stake in the international exchange for a 1pc stake - worth $39m (£24m0 based on Monday's closing price - in DFM. That would leave Nasdaq OMX facing a 70pc write-down on the current book value of its 2008 investment.

For now, the deal won't change the way the exchanges do business. They will continue to operate as separate entities which share back office functions. Over time, though, a full operational merger is probable, once some kinks - in trading currencies, regulatory standards and procedures - are ironed out.

Dubai needs creativity to pay debt without taxes

Dubai must raise funds to feed its mushrooming debt but the Gulf emirate dreads imposing taxes to avoid breaking a business model that helped turn it from a lazy fishing town to a regional trade and tourism hub.

Selling some prized assets appears to be an easier option.

Dubai, one of seven members of the United Arab Emirates federation, and state-linked firms owe an estimated $80 billion of debt borrowed to fuel a boom, when Dubai branded itself as a tax-free destination for foreign workers and businesses.

Now, scrambling to rebuild its image after a $26 billion debt bombshell last month that was poorly managed, the emirate is unlikely to risk another public relations black eye by imposing taxes at this juncture.

Selling some prized assets appears to be an easier option.

Dubai, one of seven members of the United Arab Emirates federation, and state-linked firms owe an estimated $80 billion of debt borrowed to fuel a boom, when Dubai branded itself as a tax-free destination for foreign workers and businesses.

Now, scrambling to rebuild its image after a $26 billion debt bombshell last month that was poorly managed, the emirate is unlikely to risk another public relations black eye by imposing taxes at this juncture.

Iraq’s Oil Output Quota May Become OPEC’s ‘Hot Iron’

Iraq’s plan to boost oil output with the help of foreign companies may upset the Organization of Petroleum Exporting Countries’ efforts to support prices because the nation has no quota to limit its production.

Oil companies including Royal Dutch Shell Plc, BP Plc and OAO Lukoil may help Iraq meet a target to boost oil output capacity to 12 million barrels a day in the next six years after winning oil licensing rounds earlier this year.

Oil has gained 64 percent since the beginning of 2009, when OPEC output cuts agreed late last year took effect, and is currently at about $73 a barrel. The group left production targets unchanged today at a meeting in Luanda, Angola.

Oil companies including Royal Dutch Shell Plc, BP Plc and OAO Lukoil may help Iraq meet a target to boost oil output capacity to 12 million barrels a day in the next six years after winning oil licensing rounds earlier this year.

Oil has gained 64 percent since the beginning of 2009, when OPEC output cuts agreed late last year took effect, and is currently at about $73 a barrel. The group left production targets unchanged today at a meeting in Luanda, Angola.

Kingdom to store oil in Japan

Saudi Arabia has signed a deal to put “millions of barrels” of oil in commercial storage in Japan, Minister of Petroleum and Mineral Resources Ali Al-Naimi said Tuesday.

“Asia will be a huge market and this will be a big take off,” Al-Naimi said ahead of an OPEC meeting.

About half of the Kingdom’s crude exports come to Asia, a share that is set to rise next year. Chinese state oil firms have agreed to raise 2010 crude imports from Saudi Arabia by about 12 percent from this year to top one million barrels a day, traders have said, making the world’s No. 2 oil user an important client.

“Asia will be a huge market and this will be a big take off,” Al-Naimi said ahead of an OPEC meeting.

About half of the Kingdom’s crude exports come to Asia, a share that is set to rise next year. Chinese state oil firms have agreed to raise 2010 crude imports from Saudi Arabia by about 12 percent from this year to top one million barrels a day, traders have said, making the world’s No. 2 oil user an important client.

Qatar growth to outperform key Gulf economies on gas

Qatar’s nominal GDP grew 11% in the third quarter compared with Q3, 2008 and totalled QR75.5bn, the Qatar Statistics Authority said yesterday.

“The gas sector recovered from the decline seen in the first half of 2009 due to price rises seen for all major commodities,” the QSA said.

The contribution from the oil sector grew due to the average price of crude oil rising from $60 a barrel to $68 a barrel.

“The gas sector recovered from the decline seen in the first half of 2009 due to price rises seen for all major commodities,” the QSA said.

The contribution from the oil sector grew due to the average price of crude oil rising from $60 a barrel to $68 a barrel.

BAHRAIN LEADS MENA REGION IN ECONOMIC FREEDOM

ACCORDING TO THE ANNUAL INDEX OF ECONOMIC FREEDOM, PUBLISHED BY THE HERITAGE FOUNDATION AND WALL STREET JOURNAL, BAHRAIN IS THE 13TH FREEST ECONOMY IN THE WORLD, AND THE MOST FREE IN THE MIDDLE EAST AND NORTH AFRICA (MENA) REGION.

IT IS TO BE NOTED THAT BAHRAIN IS THE ONLY ECONOMY IN THE MENA REGION TO RANK AMONG THE WORLD'S TOP 20 FOR THE 16TH CONSECUTIVE YEAR SINCE THE INDEX WAS FIRST LAUNCHED IN 1995. THE REPORT ACCOMPANYING THE INDEX NOTED THAT THE GCC REGION REMAINS CENTRAL TO WORLD ECONOMY. BAHRAIN'S 13TH POSITION IS AN IMPROVEMENT ON ITS PREVIOUS 16TH POSITION, WITH GAINS IN VARIOUS FIELDS FOCUSED ON BY THE INDEX SUCH AS INVESTMENT FREEDOM, TRADE FREEDOM, LABOUR FREEDOM, AND FREEDOM FROM CORRUPTION. MORE.......... WHQ 22-DEC-2009 20:06 COMMENTING ON SUCH POSITIVE RESULTS, ECONOMIC DEVELOPMENT BOARD (EDB) CHIEF EXECUTIVE SHAIKH MOHAMMED BIN ISA AL KHALIFA SAID THAT GROWTH HAS BEEN STIMULATED BY A COMPREHENSIVE ECONOMIC REFORM PROJECT LAUNCHED BY HRH PRINCE SALMAN BIN HAMAD AL KHALIFA, THE CROWN PRINCE AND EDB CHAIRMAN, THROUGH HIS COMMITMENT TOWARDS HUMAN CAPITAL, DIVERSIFICATION AND TRANSPARENT REGULATION. EDB IS WORKING WITH STAKEHOLDERS IN BOTH THE PRIVATE AND PUBLIC SECTORS IN BAHRAIN TO BRING ABOUT A CHANGE PROCESS THAT IS INEXTRICABLY LINKED TO THE TASK OF MAKING BAHRAIN ONE OF THE FREEST ECONOMIES IN THE WORLD - A PLACE IN WHICH OUR BUSINESSES, OUR CITIZENS AND OUR SOCIETY CAN THRIVE, HE ADDED. WE ARE PROUD OUR ACHIEVEMENTS HAVE BEEN REFLECTED AND ENDORSED BY HIGHLY REGARDED INSTITUTIONS SUCH AS THE HERITAGE FOUNDATION AND THE WALL STREET JOURNAL, HE ALSO SAID. THE FACT THAT THIS PROGRESS HAS BEEN TRANSLATED INTO ECONOMIC GROWTH ALSO REFLECTS THE REALITY THAT THE REFORMS BEING DRIVEN BY THE EDB AND OTHER ORGANISATIONS IN BAHRAIN ARE TRULY HELPING PRIVATE AND PUBLIC SECTOR ENTITIES TO THRIVE, HE NOTED. WHQ 22-DEC-2009 20:08

IT IS TO BE NOTED THAT BAHRAIN IS THE ONLY ECONOMY IN THE MENA REGION TO RANK AMONG THE WORLD'S TOP 20 FOR THE 16TH CONSECUTIVE YEAR SINCE THE INDEX WAS FIRST LAUNCHED IN 1995. THE REPORT ACCOMPANYING THE INDEX NOTED THAT THE GCC REGION REMAINS CENTRAL TO WORLD ECONOMY. BAHRAIN'S 13TH POSITION IS AN IMPROVEMENT ON ITS PREVIOUS 16TH POSITION, WITH GAINS IN VARIOUS FIELDS FOCUSED ON BY THE INDEX SUCH AS INVESTMENT FREEDOM, TRADE FREEDOM, LABOUR FREEDOM, AND FREEDOM FROM CORRUPTION. MORE.......... WHQ 22-DEC-2009 20:06 COMMENTING ON SUCH POSITIVE RESULTS, ECONOMIC DEVELOPMENT BOARD (EDB) CHIEF EXECUTIVE SHAIKH MOHAMMED BIN ISA AL KHALIFA SAID THAT GROWTH HAS BEEN STIMULATED BY A COMPREHENSIVE ECONOMIC REFORM PROJECT LAUNCHED BY HRH PRINCE SALMAN BIN HAMAD AL KHALIFA, THE CROWN PRINCE AND EDB CHAIRMAN, THROUGH HIS COMMITMENT TOWARDS HUMAN CAPITAL, DIVERSIFICATION AND TRANSPARENT REGULATION. EDB IS WORKING WITH STAKEHOLDERS IN BOTH THE PRIVATE AND PUBLIC SECTORS IN BAHRAIN TO BRING ABOUT A CHANGE PROCESS THAT IS INEXTRICABLY LINKED TO THE TASK OF MAKING BAHRAIN ONE OF THE FREEST ECONOMIES IN THE WORLD - A PLACE IN WHICH OUR BUSINESSES, OUR CITIZENS AND OUR SOCIETY CAN THRIVE, HE ADDED. WE ARE PROUD OUR ACHIEVEMENTS HAVE BEEN REFLECTED AND ENDORSED BY HIGHLY REGARDED INSTITUTIONS SUCH AS THE HERITAGE FOUNDATION AND THE WALL STREET JOURNAL, HE ALSO SAID. THE FACT THAT THIS PROGRESS HAS BEEN TRANSLATED INTO ECONOMIC GROWTH ALSO REFLECTS THE REALITY THAT THE REFORMS BEING DRIVEN BY THE EDB AND OTHER ORGANISATIONS IN BAHRAIN ARE TRULY HELPING PRIVATE AND PUBLIC SECTOR ENTITIES TO THRIVE, HE NOTED. WHQ 22-DEC-2009 20:08

How badly has the debt crisis damaged Dubai’s reputation?

Looking back over the past couple of months you have to wonder how much Dubai has damaged its reputation as a growing global financial centre. The headlines suggesting that the city is drowning in debt are not positive, and the reality that has emerged is not that great either.

Before the debt crisis the reputation of the Dubai International Financial Centre was definitely rising fast. A report commissioned by the DIFC from KPMG, and published today but presumably with field work from before the Dubai debt crisis, showed Dubai seventh ahead of Frankfurt in a competitiveness league table of financial centres:

1. Singapore

2. London (UK)

3. New York (USA)

4. Hong Kong

5. Zurich (Switzerland)

6. Tokyo (Japan)

7. Dubai International Financial Centre (UAE)

8. Frankfurt (Germany)

9. Luxembourg

10. Dubai (UAE)

11. Paris (France)

12. Dublin (Ireland)

13. Doha (Qatar)

14. Manama (Bahrain)

15. Riyadh (Saudi Arabia)

High ranking

A press release from the DIFC said it was ranked this highly ‘on the strength of its world-class legal and regulatory standards; independent regulator and judiciary system; and strong value offering for financial businesses. DIFC’s infrastructure and business environment, custom-designed for the financial industry, also helped Dubai receive an overall competitiveness score higher than global centres like Paris and Dublin.

‘The report assesses the competitiveness of financial centres using an evaluation model that measures both ‘capability’ factors or immediate benefits provided by a financial centre, and ‘performance’ factors, which reflect historical or long-term results. The focus on ‘competitiveness’ puts the spotlight on the potential of a centre to excel in the future and not just on its current status.

‘The final rankings were based on a composite score derived from three pillars – Industry Opinion, Industry Performance, and Capability Measurement – that determines overall competitiveness.

‘The Industry Opinion pillar is based on the Global Financial Centres Index 6 published by the City of London, while the Industry Performance pillar is based on the Financial Development Index 2009 published by the World Economic Forum.

‘The Capability Measurement pillar is based on an assessment model developed to measure the growth potential of a financial centre in the future based on a three factors including business environment, cost of doing business and cost of living.’

Reputation damaged

However, any observer from the financial sector is bound to ask whether the ‘Industry Opinion pillar’ is not likely to have changed significantly in the wake of the Dubai debt crisis of the past two months. Certainly the risk perception of lending to Dubai must have been transformed.

But the global financial community are pragmatic folk. Dubai did not actually default on its Islamic bond this month. There is a rescheduling of $22 billion in debt owed by Dubai World subsidiaries Nakheel and Limitless now in progress. That is probably the biggest debt problem facing Dubai but there will be others.

So whether the Dubai debt crisis does significant long-term damage to its global financial reputation is likely a matter of how it proceeds from here. Greater transparency and openness and a willingness to discuss past mistakes is a step forward, so too is the merger of the two Dubai stock market trading floors announced today.

Dubai will also have to learn how to handle the global media with effective public relations and abandon its high-handed approach to the press. But all is not lost. The same banks that suffered in the Russian default of 1998 were back lending again within a few years. Reputations can be mended pretty fast when there is business to be done.

Before the debt crisis the reputation of the Dubai International Financial Centre was definitely rising fast. A report commissioned by the DIFC from KPMG, and published today but presumably with field work from before the Dubai debt crisis, showed Dubai seventh ahead of Frankfurt in a competitiveness league table of financial centres:

1. Singapore

2. London (UK)

3. New York (USA)

4. Hong Kong

5. Zurich (Switzerland)

6. Tokyo (Japan)

7. Dubai International Financial Centre (UAE)

8. Frankfurt (Germany)

9. Luxembourg

10. Dubai (UAE)

11. Paris (France)

12. Dublin (Ireland)

13. Doha (Qatar)

14. Manama (Bahrain)

15. Riyadh (Saudi Arabia)

High ranking

A press release from the DIFC said it was ranked this highly ‘on the strength of its world-class legal and regulatory standards; independent regulator and judiciary system; and strong value offering for financial businesses. DIFC’s infrastructure and business environment, custom-designed for the financial industry, also helped Dubai receive an overall competitiveness score higher than global centres like Paris and Dublin.

‘The report assesses the competitiveness of financial centres using an evaluation model that measures both ‘capability’ factors or immediate benefits provided by a financial centre, and ‘performance’ factors, which reflect historical or long-term results. The focus on ‘competitiveness’ puts the spotlight on the potential of a centre to excel in the future and not just on its current status.

‘The final rankings were based on a composite score derived from three pillars – Industry Opinion, Industry Performance, and Capability Measurement – that determines overall competitiveness.

‘The Industry Opinion pillar is based on the Global Financial Centres Index 6 published by the City of London, while the Industry Performance pillar is based on the Financial Development Index 2009 published by the World Economic Forum.

‘The Capability Measurement pillar is based on an assessment model developed to measure the growth potential of a financial centre in the future based on a three factors including business environment, cost of doing business and cost of living.’

Reputation damaged

However, any observer from the financial sector is bound to ask whether the ‘Industry Opinion pillar’ is not likely to have changed significantly in the wake of the Dubai debt crisis of the past two months. Certainly the risk perception of lending to Dubai must have been transformed.

But the global financial community are pragmatic folk. Dubai did not actually default on its Islamic bond this month. There is a rescheduling of $22 billion in debt owed by Dubai World subsidiaries Nakheel and Limitless now in progress. That is probably the biggest debt problem facing Dubai but there will be others.

So whether the Dubai debt crisis does significant long-term damage to its global financial reputation is likely a matter of how it proceeds from here. Greater transparency and openness and a willingness to discuss past mistakes is a step forward, so too is the merger of the two Dubai stock market trading floors announced today.

Dubai will also have to learn how to handle the global media with effective public relations and abandon its high-handed approach to the press. But all is not lost. The same banks that suffered in the Russian default of 1998 were back lending again within a few years. Reputations can be mended pretty fast when there is business to be done.

Subscribe to:

Comments (Atom)