Value Stocks Beckon in Emerging Markets | PRAGMATIC CAPITALISM:

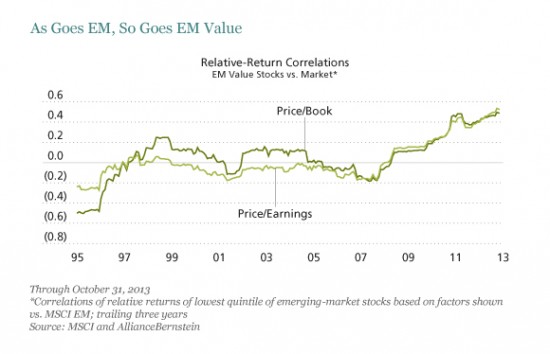

"Years of playing defense have left many emerging-market (EM) equity portfolios laden with pricey safe-haven stocks. We think they risk missing the big opportunity that’s brewing in value stocks, especially as EM economies begin to stabilize.

The risk rally that has thundered across the developed markets (DM) over the past 18 months has largely bypassed the emerging world. Emerging economies have responded more slowly than usual to improving DM activity, while uncertainties about rich-world monetary policies loom. Nervous EM investors have been slow to abandon the relative safety of predictable, fundamentally stable stocks, while shunning riskier stocks—regardless of valuation.

We think it’s time for a rethink. Nearly two-thirds of actively managed EM equity assets are in stocks trading at premiums to the market of 10% or higher, with the largest portion skewed to those with premiums above 20% (Display 1). This is a big change from the past. As recently as 2006, allocations had been more evenly dispersed between expensive and cheap stocks, following a lengthy stretch of value outperformance in the wake of the bursting of the tech bubble.

"

"

'via Blog this'

"Years of playing defense have left many emerging-market (EM) equity portfolios laden with pricey safe-haven stocks. We think they risk missing the big opportunity that’s brewing in value stocks, especially as EM economies begin to stabilize.

The risk rally that has thundered across the developed markets (DM) over the past 18 months has largely bypassed the emerging world. Emerging economies have responded more slowly than usual to improving DM activity, while uncertainties about rich-world monetary policies loom. Nervous EM investors have been slow to abandon the relative safety of predictable, fundamentally stable stocks, while shunning riskier stocks—regardless of valuation.

We think it’s time for a rethink. Nearly two-thirds of actively managed EM equity assets are in stocks trading at premiums to the market of 10% or higher, with the largest portion skewed to those with premiums above 20% (Display 1). This is a big change from the past. As recently as 2006, allocations had been more evenly dispersed between expensive and cheap stocks, following a lengthy stretch of value outperformance in the wake of the bursting of the tech bubble.

'via Blog this'

No comments:

Post a Comment